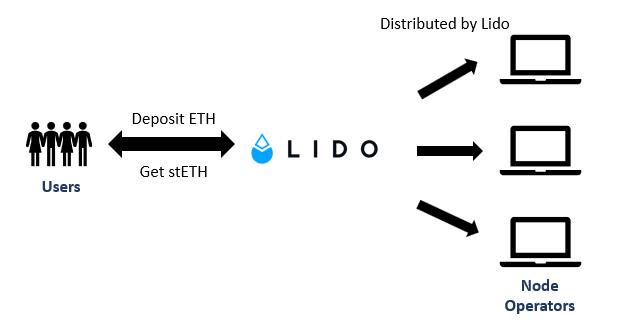

Mechanisms: Once users stake their ETH, Lido will distribute deposited ETH to permissioned node operators (validators) in Lido, meaning becoming a node operator requires DAO voting. As of 3Q2022, Lido has 27 node operators. For providing the liquid staking service, Lido charges a 10% fee on a users’ staking reward. The fee will be split between the node operator and Lido DAO.

Once users are finished staking, they will receive equivalent ETH and enjoy rewards of 4.9% APR, which will dynamically change over time, as of now.

1) stETH: Every 12PM UTC, stETH token balances will update, depending on changes in ETH deposited and changes in ETH rewards from users who stake via Lido. Because the rewards are embodied through a balance rebase, users should see their stETH balance automatically change without an accompanying transaction taking place. This mechanism is called rebasing.

2) APR: APR varies from time to time, which is affected by 1) Consensus layer reward: how many ETH are staked in the consensus layer. The more ETH is staked, the less rewards can be obtained from the consensus layer. 2) Execution layer reward: Node operators get MEV and transaction priority fees, which rely on on-chain activities.

Source: Crypto_Lai

Ecosystem

- stETH and wstETH: Since stETH is a rebasing token, there will be some compatibility issues in certain DeFi and L2 protocols. As a result, Lido issues the stETH wrapped token, wstETH, which will not automatically reflect the updated amount in users’ wallet.

- Wallet: In Jan 2023, MetaMask announced it will allow users to stake ETH through MetaMask Portfolio dapp, providing a better UI/UX for liquid staking.

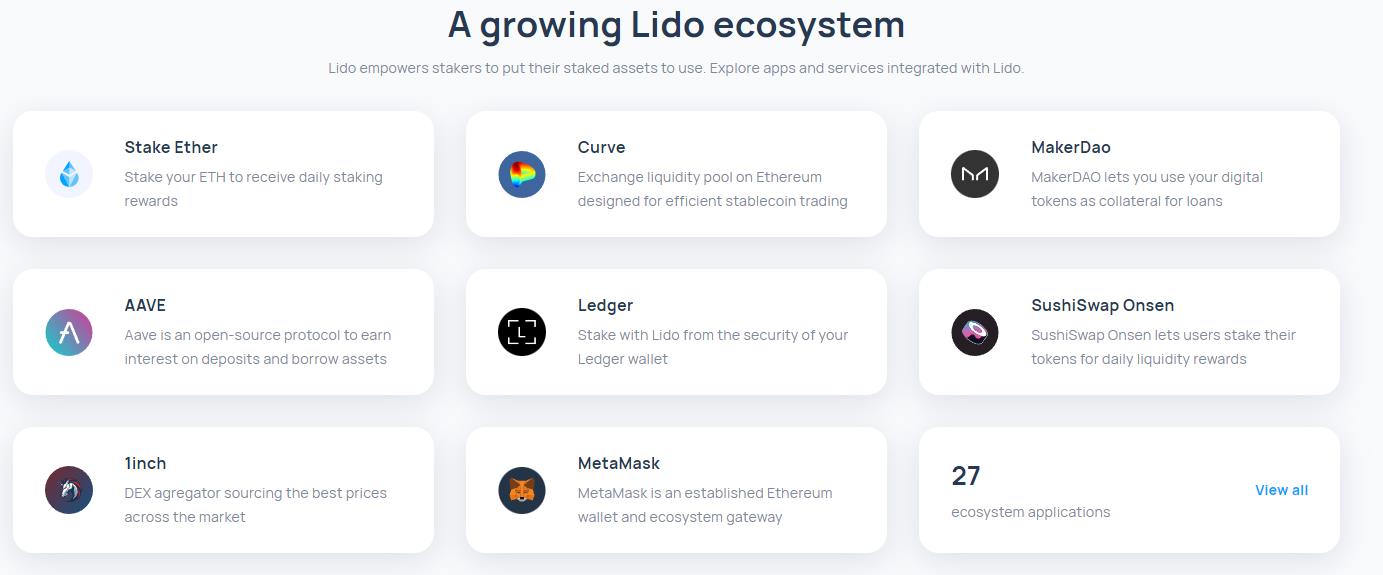

- DeFi: As one of the early liquid staking projects, Lido’s stETH is widely applied in top DeFi protocols, including:

- Curve (steth pool): The largest pool in Curve in terms of TVL (USD $1.6 bn)

- AAVE: stETH can be deposited in AAVE V2, and be used as collateral for further borrowing.

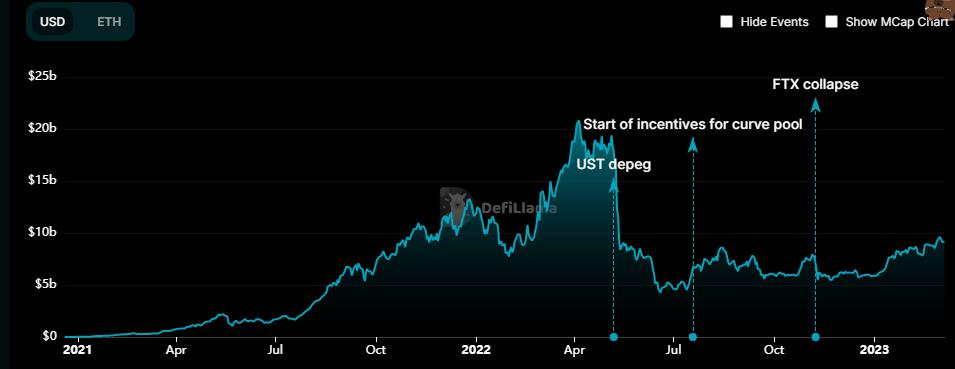

Operational performance

Lido currently is the largest DeFi protocol in terms of TVL (USD 9.18bn)

Source: DefiLlama

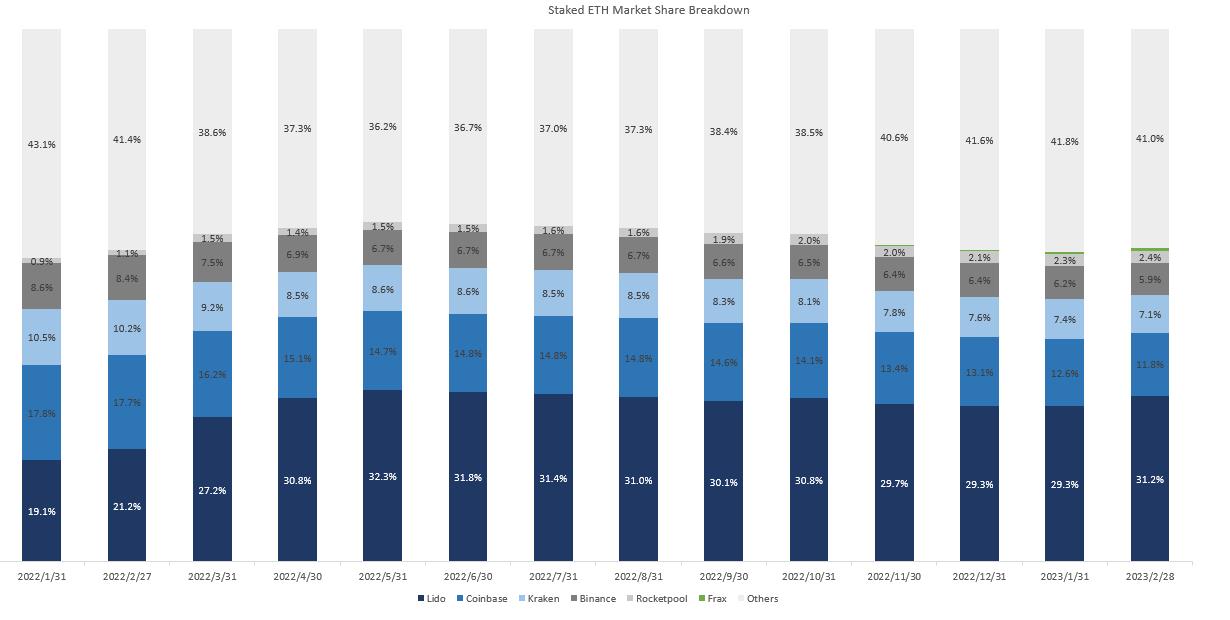

Although market share of staked ETH slightly decreased since July 2022, Lido still remains the largest liquid staking protocol while the second (Coinbase) and the third (Kraken) players are centralized exchanges. In Febryart 2023, Lido’s market share jumped from 29.3% from January to 31.2% in February 2023 as a cryptocurrency entrepreneur Justin Sun staked more than 300,000 ETH in Lido.

Source: Dune Analytics and Crypto_Lai

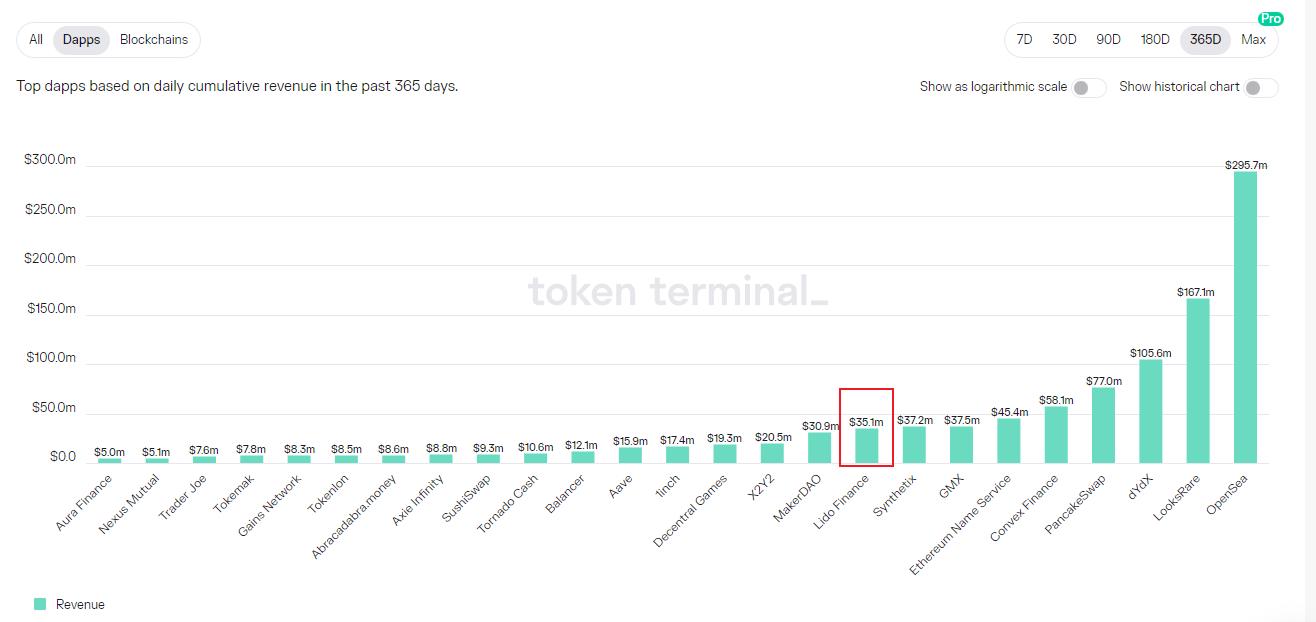

According to tokenterminal, Lido ranked 9th across all dapps in the crypto space and 1st in the liquid staking sector in terms of revenue generating capabilities in the past 365 days.

Source: Token Terminal

Investors

Opportunities

- Shanghai upgrade to further drive overall ETH liquid staking: The Shanghai upgrade of Ethereum is expected to launch in April 2023, aiming to enable the withdrawal function. Once it is successfully implemented, users can deposit and withdraw ETH freely. It is estimated by several crypto research firms that the withdrawal function will increase the ETH staking ratio as concern of liquidity control will be mitigated. Currently, only 13% of total ETH is staked, which is lower than that of other PoS blockchain, such as Cardano (72%), Solana (71%), Avalanche (62%), Cosmos (62%), Polygon (39%), representing a huge market upside potential.

Some would wonder if users who staked their ETH at an earlier time would unstake and sell their ETH when the withdrawal function is enabled, creating selling pressure. However, the unlock is gradually fulfilled instead of unstaking all at once. Currently, it is estimated that the daily withdrawal limit is around 55,000ETH. Under this assumption, it will take 299 days to unstake all ETH based on the current number.

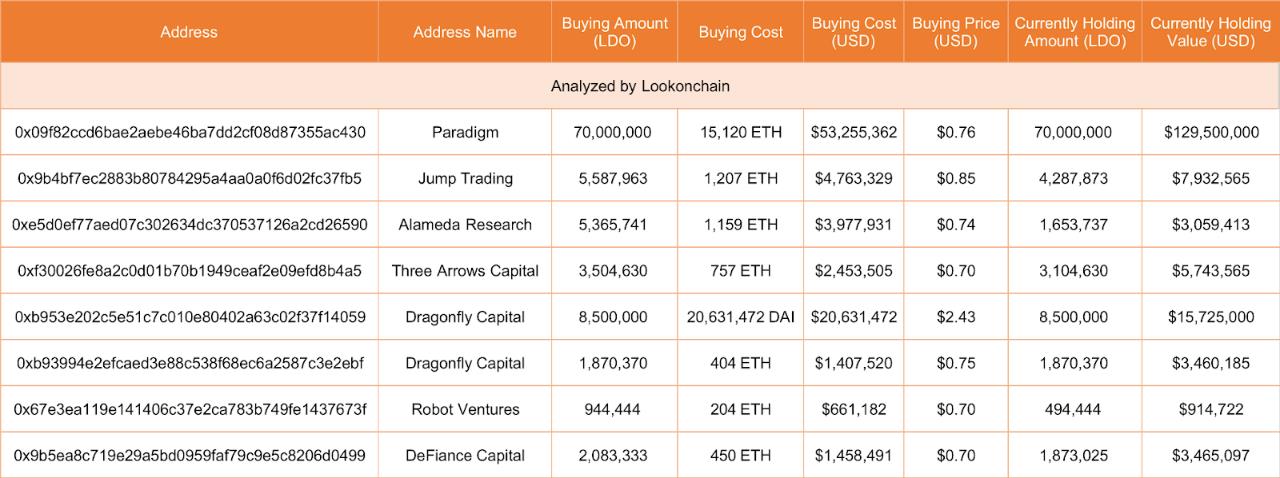

Diamond hands: Lido’s price performance has been strong since 2023. During the price spike, many VCs started to sell their tokens. It can be expected that VCs who did not sell in the beginning of Jan 2023 are more likely to stay in the long run.

Source: Lookonchain

- More decentralized initiatives: One of the disadvantages of Lido is that being a validator requires permission. With the introduction of DVT, it could become more decentralized in the future, meaning better security.

Risks

- Intensified competition: Despite having significant market share, Lido has faced intensified competition from other decentralized peers. Examples are Rocketpool and Frax, and both utilize more decentralized approaches to running node operators and are more involved in other ecosystem. Lido’s market share increase primarily came from one individual in Feb 2023, and is actually losing market share from Jul 2022 to Jan 2023.

- Token function: The LDO token only has governance and incentive functions, which is not directly linked to the operating performance of the protocol.

- Mechanism of withdrawal is unknown: Currently, the withdrawal specification is not finalized. When Ethereum’s withdrawal specification is finalized, Lido will prepare a new contract and initiate a vote among LDO holders for the upgrade. Although unlikely, the risk of unsuccessful implementation can’t be ruled out.

- Depeg: As stETH’s price is pegged to ETH, there isa possibility that stETH depegs (i.e. losing 1:1 ratio), especially when the crypto market experiences huge price decline or deleveraging.

- Regulation: In Feb 2023, SEC charged Kraken with a $30mn fine as a result of failing to register their crypto asset staking-as-a-service program. Given the SEC’s aggressive actions recently, it is uncertain how decentralized staking platforms will be impacted.

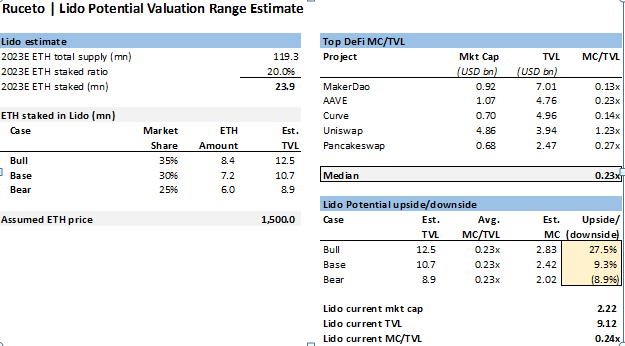

Illustrative Valuation

An illustrative valuation LDO ranges from (8.9%) – 27.5% based on the following assumptions:

- 2023E ETH total supply is 119.3mn

- 2023E ETH staked ratio can potentially rise to 20% (from 13%) by the end of 2023 from the Shanghai upgrade.

- Lido’s market share might range from 25%-35%. Liquid staking market can potentially expand due to the Shanghai upgrade, but competition will also intensify. Base case is Lido maintaining its market share of approximately 30%.

- ETH price: USD 1500

Currently, Lido’s MC/TVL is around 0.24x, around the same as the median peer multiple of 0.23x. There is a possibility that Lido will trade closer to Uniswap’s 1.23x multiple in the long run due to:

- Lido’s leading position in the liquid staking sector

- As the Shanghai upgrade completes, liquid staking protocols will play a more important role in DeFi as well as liquidity aggregation.